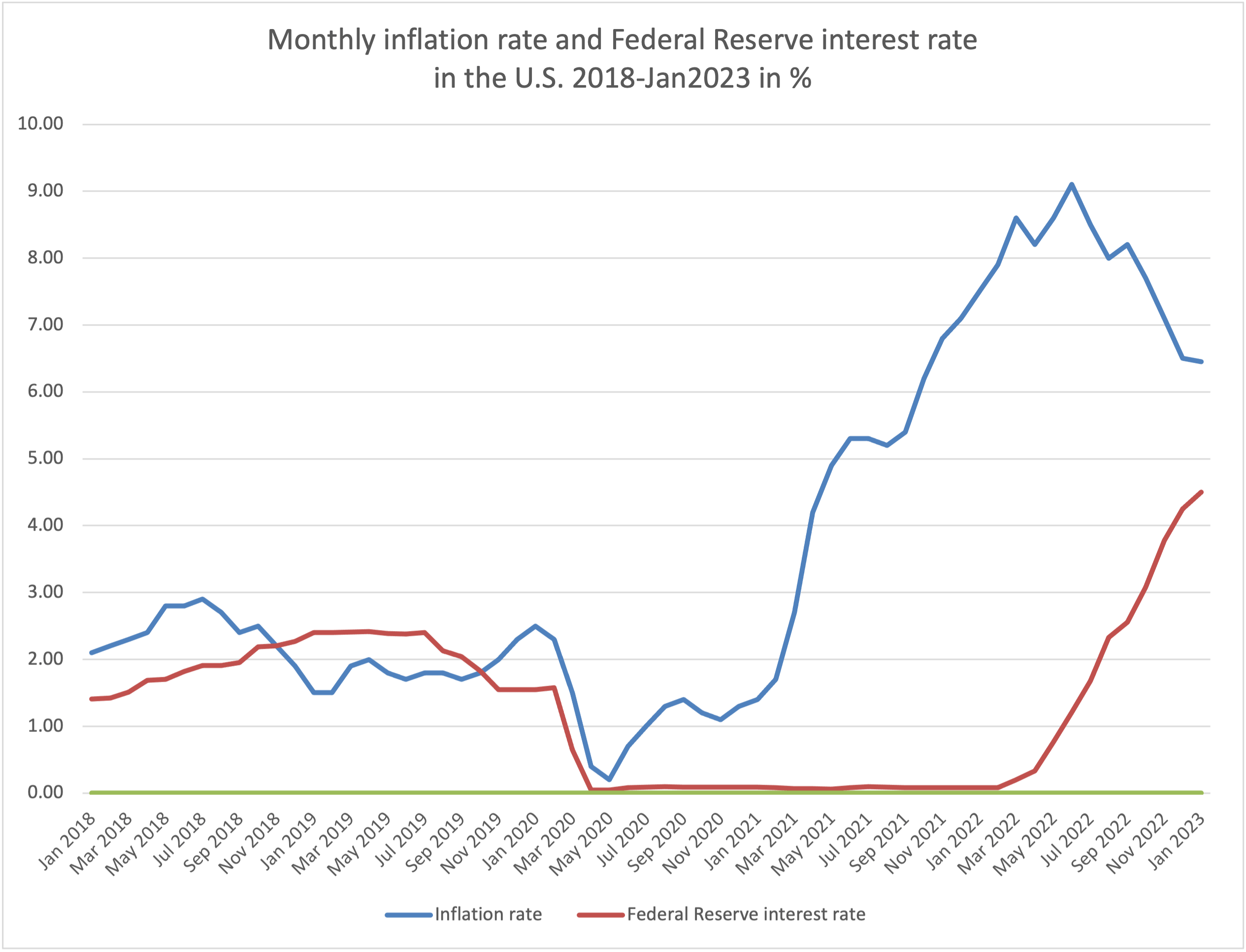

The era of predictable money is dead. For decades, the global economy operated under a simple, almost theological assumption: inflation was a ghost of the 1970s and interest rates would hover near zero indefinitely. That illusion shattered in 2022, and the wreckage is still being cleared in 2026. While the headlines suggest a "return to normal," the reality is a fragmented global landscape where the cost of living and the price of debt are diverging wildly between neighbors.

The primary query for any observer today is whether the fever has finally broken. The answer is a qualified yes, but the recovery is uneven and painful. Global headline inflation is projected to settle at approximately 3.7% for 2026, down from the harrowing peaks of previous years. However, this average masks a visceral divide. While the United States battles "sticky" service inflation at 2.4%, and the Eurozone flirts with a 1.7% floor, countries like Argentina and Turkey remain trapped in a hyper-inflationary spiral that exceeds 30%.

The Great Divergence of 2026

Central banks are no longer moving in lockstep. In the immediate aftermath of the pandemic, the world's monetary authorities acted like a single, massive organism, raising rates in a desperate attempt to quash surging prices. Today, that unity has evaporated. We are witnessing a "Great Divergence" where domestic politics and regional energy dependencies dictate the value of your paycheck.

In the United States, the Federal Reserve has hit a wall. Despite three rate cuts in 2025 that brought the benchmark federal funds rate to a range of 3.5% to 3.75%, the "last mile" of disinflation is proving treacherous. The American consumer, bolstered by a resilient labor market, continues to spend. This prevents inflation from hitting the Fed's 2% target, forcing Jerome Powell and his colleagues to maintain a stance that is "higher for longer" compared to their European counterparts.

Conversely, the Bank of England and the European Central Bank (ECB) are facing a different demon: stagnation. With inflation in the Euro area expected to dip below 2% by mid-2026, the pressure to cut rates further is immense. Germany, once the engine of Europe, is sputtering, and the high cost of borrowing is now viewed as a greater threat to stability than the rising price of bread.

The Real Interest Rate Trap

To understand why your mortgage feels heavier even as "inflation falls," you must distinguish between nominal and real interest rates. The nominal rate is the number the bank tells you; the real rate is that number minus inflation. In 2026, real interest rates in the US and UK remain elevated at roughly 1.2% to 2.1%.

This is a deliberate squeeze. Central banks are keeping real rates positive to ensure inflation doesn't roar back, but the collateral damage is the "debt-servicing trap." Governments and corporations that gorged on cheap debt in 2019 are now forced to refinance at double or triple the cost. The OECD reports that 78% of government borrowing in 2026 will go simply toward paying off old debt. It is a treadmill that is moving faster than the economies it supports.

The Hidden Drivers of the 2026 Price Surge

If supply chains have healed, why is life still so expensive? The investigative reality is that the "why" has shifted from temporary bottlenecks to structural shifts.

- The AI Capex Race: The massive shift toward artificial intelligence is not just a tech trend; it is a macro-economic force. Nine major tech players are projected to borrow over $1.2 trillion by 2030 to fund AI infrastructure. This massive demand for capital keeps long-term bond yields high, preventing interest rates for the average consumer from falling back to the "easy money" levels of the 2010s.

- Protectionism as a Tax: The trade wars have evolved. Tariffs are no longer just political theater; they are a permanent fixture of the 2026 economy. These "border adjustments" act as a direct tax on consumers, keeping goods prices high in the US while redirecting cheaper Chinese exports to other regions, further widening the gap between domestic and international prices.

- The Labor Power Shift: Wage growth in Japan is finally moving higher after decades of hibernation. While good for workers, it forces the Bank of Japan to abandon its negative interest rate experiments, removing one of the last anchors of global cheap liquidity.

The Winners and Losers of the New Map

The tracking of these rates reveals a stark hierarchy of economic survival.

| Country | Inflation (Feb 2026) | Central Bank Rate | The Reality Check |

|---|---|---|---|

| United States | 2.4% | 3.6% | Sticky services; Fed remains cautious. |

| Germany | 1.9% | 3.0% (ECB) | Disinflation is here, but growth is missing. |

| Japan | 1.5% | 0.25% | The end of the "free money" era for the world. |

| Switzerland | 0.1% | 1.0% | The ultimate safe haven; deflation is the new risk. |

| Argentina | 32.4% | 40%+ | Total currency collapse; rates are irrelevant. |

The Debt Tsunami

The most overlooked factor in the current interest rate tracker is the sheer volume of public debt. Global public debt is approaching 100% of world GDP. In 2026, we are entering a "fiscal dominance" phase where central banks might be forced to keep rates lower than they should—not because inflation is gone, but because the government cannot afford the interest payments on its own debt.

This creates a "zombie economy" where interest rates are too high to encourage new business but too low to actually kill off inflation. It is a precarious balance. If a major economy like Italy or a secondary US state faces a credit crunch, the central banks will have to choose: let the system collapse or print money and spark another wave of inflation.

The Survival Strategy

For the individual, the takeaway is concrete. The era of 3% fixed-rate mortgages is a historical anomaly that is not returning. In the 2026 landscape, cash is once again a viable asset, and debt is a dangerous liability.

Investors are shifting toward "price-sensitive" assets. As central banks reduce their bond holdings, markets have become more volatile. We are seeing a shift where hedge funds and households, rather than institutions, are the primary buyers of government debt. This makes the system more prone to "flash crashes" and sudden spikes in borrowing costs.

The data suggests that the "soft landing" so many hoped for is more of a "hard grind." Prices are not going back to 2019 levels. They are merely rising more slowly from a much higher base. The interest rate tracker isn't just a list of numbers; it is a map of where the next sovereign crisis will likely ignite.

Check your local bank's latest prime rate adjustment today—it tells you more about your future than any political promise.