The headlines are screaming about a "rebound." They see a Purchasing Managers' Index (PMI) ticking above 50 and they break out the champagne. They tell you the Chinese dragon is breathing fire again because factory floors are humming at their "fastest pace in a year."

They are wrong. They are looking at a speedometer while the engine is overheating and the steering column is snapping in half.

The consensus view—that expanding factory activity signals a healthy recovery—is a dangerous simplification. In reality, what we are witnessing isn't a resurgence of organic demand. It is a desperate, state-subsidized supply-side surge that is decoupled from actual global consumption. We aren't seeing a "growth" story; we are seeing the beginning of a global trade war fueled by overcapacity that the world can no longer absorb.

The Ghost of 50.1

The PMI is a diffusion index. It measures the direction of change, not the absolute magnitude of health. When a state-aligned report shows a reading of 50.8 or 51.1, the "market experts" treat it as a victory. I have spent two decades analyzing supply chains from Shenzhen to Stuttgart, and I can tell you: a factory running at 100% capacity to produce goods no one is buying is a liability, not an asset.

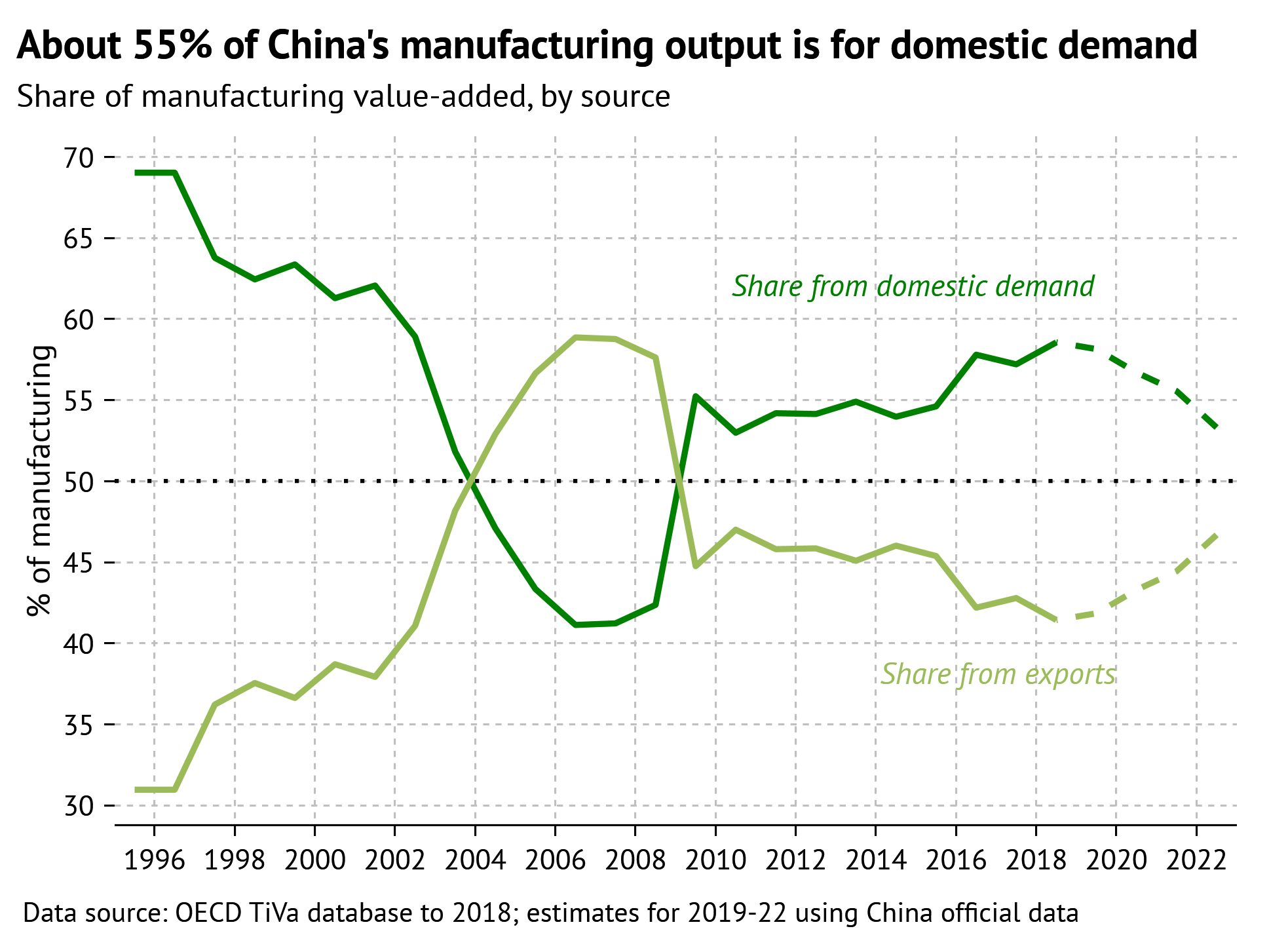

The current "expansion" is driven by a massive pivot. With the Chinese property market—formerly 25% to 30% of their GDP—in a structural death spiral, Beijing has doubled down on the only lever they know how to pull: manufacturing. They are shoving capital into "new three" industries: electric vehicles, lithium-ion batteries, and solar products.

But here is the logic gap the mainstream media ignores: Who is buying this stuff?

Internal Chinese consumption is anemic. Retail sales are lagging. Household wealth is tied up in unfinished apartments. When a country produces far more than its citizens can consume, it must export the difference. This isn't growth; it's an eviction of domestic economic problems onto the doorsteps of the rest of the world.

The High Cost of "Cheap"

Mainstream analysts love to talk about "competitiveness." They claim China’s factory strength comes from sheer efficiency. That is a myth. The "expansion" we see is lubricated by a banking system that prioritizes state-owned enterprises (SOEs) and strategic sectors over actual profitability.

Imagine a scenario where you run a widget factory. Your costs are $10. The market price is $8. In a rational economy, you go bust. In the current Chinese "expansion" model, the state gives you a low-interest loan to build a second factory so you can produce widgets for $7 through sheer scale, hoping to bankrupt your global competitors before your debt matures.

This is "profitless prosperity." It shows up as a positive PMI number, but it’s a cancer on the balance sheet.

- Inventory Stacking: Much of this reported growth is actually just inventory buildup. Factories are producing to meet state targets, not purchase orders.

- Price Deflation: Chinese producer prices have been in negative territory for months. If you are producing more but charging less, you aren't growing—you are liquidating.

- The Subsidy Trap: When the state dictates where capital goes, it creates "zombie" sectors. We saw this in steel. We saw it in aluminum. We are seeing it now in EVs.

Dismantling the "People Also Ask" Delusions

If you search for news on China's economy, the questions being asked reveal a fundamental misunderstanding of how global trade works in 2026.

"Is China's economy finally recovering?"

No. A recovery implies a return to a balanced state. This is a transformation into a hyper-producer. You cannot recover by building more factories when your biggest problem is that you already have too many factories and not enough customers.

"Will this manufacturing surge help global inflation?"

In the short term, yes, because China is exporting deflation. In the long term, no. By flooding markets with subsidized goods, they are forcing Western manufacturers to shut down. Once the competition is gone and trade barriers go up—and they are going up—prices will skyrocket.

"Should I invest in Chinese manufacturing stocks now?"

Only if you enjoy catching falling knives. Growth in output does not equal growth in shareholder value when the primary objective is national employment and strategic dominance, not dividends.

The Coming Collision

The "lazy consensus" says that a busy China is good for the world. That was true in 2004. It is a fantasy in 2026.

The world’s "absorptive capacity" for Chinese exports has hit a hard ceiling. The US, the EU, Brazil, and even India are erecting walls. Section 301 tariffs, anti-dumping probes, and "Foreign Entity of Concern" rules are not just political theater—they are a systemic immune response.

When you read that "factory activity expanded at its sharpest pace," you should be reading: "Trade tensions are about to hit a breaking point."

I’ve watched companies move their entire operations out of the Pearl River Delta because they saw this coming. They realized that a factory floor that never sleeps is a terrifying sight when the warehouse next door is full of unsold stock. The "sharpest pace" is the sound of a train accelerating toward a wall.

The Strategy for the Contrarian Leader

Stop looking at the PMI as a signal to buy or a signal of "health." Start looking at it as a signal of impending volatility.

- Diversify Away from the Surge: If your supply chain relies on these "expanding" sectors, you are one executive order away from a total shutdown. The more China pushes these exports, the faster the West will ban them.

- Watch Input Prices, Not Output Volume: The real story isn't that they are making more; it’s that the cost of raw materials is rising while their finished goods prices are falling. That margin squeeze is where the truth lives.

- Ignore the "Soft Landing" Narrative: There is no soft landing for a manufacturing sector that is being used as a social welfare program to keep people employed.

The headlines are celebrating a pulse. They haven't realized it's the pulse of a fever.

Don't mistake motion for progress. A spinning tire in the mud has plenty of motion; it just isn't going anywhere except deeper into the hole. The next time you see a report praising China's "resilient" factory data, remember that a bridge also looks most "resilient" right before the resonance frequency tears it apart.

The "expansion" isn't the story. The inevitable, violent correction is.