The stability of China’s internal economy depends on a delicate equilibrium between its Strategic Petroleum Reserve (SPR) capacity and the volatility of the Strait of Hormuz. While market observers often focus on spot price fluctuations during Middle Eastern kinetic conflicts, the true analytical floor is the import dependency ratio, which for China remains stubbornly above 70%. An escalation in Iran does not merely threaten a price spike; it threatens the physical continuity of the "Teapot" refinery ecosystem in Shandong and the broader industrial output of the Yangtze River Delta.

The Triad of Chinese Energy Vulnerability

China's energy security during an Iranian conflict is governed by three interconnected variables that define its operational runway.

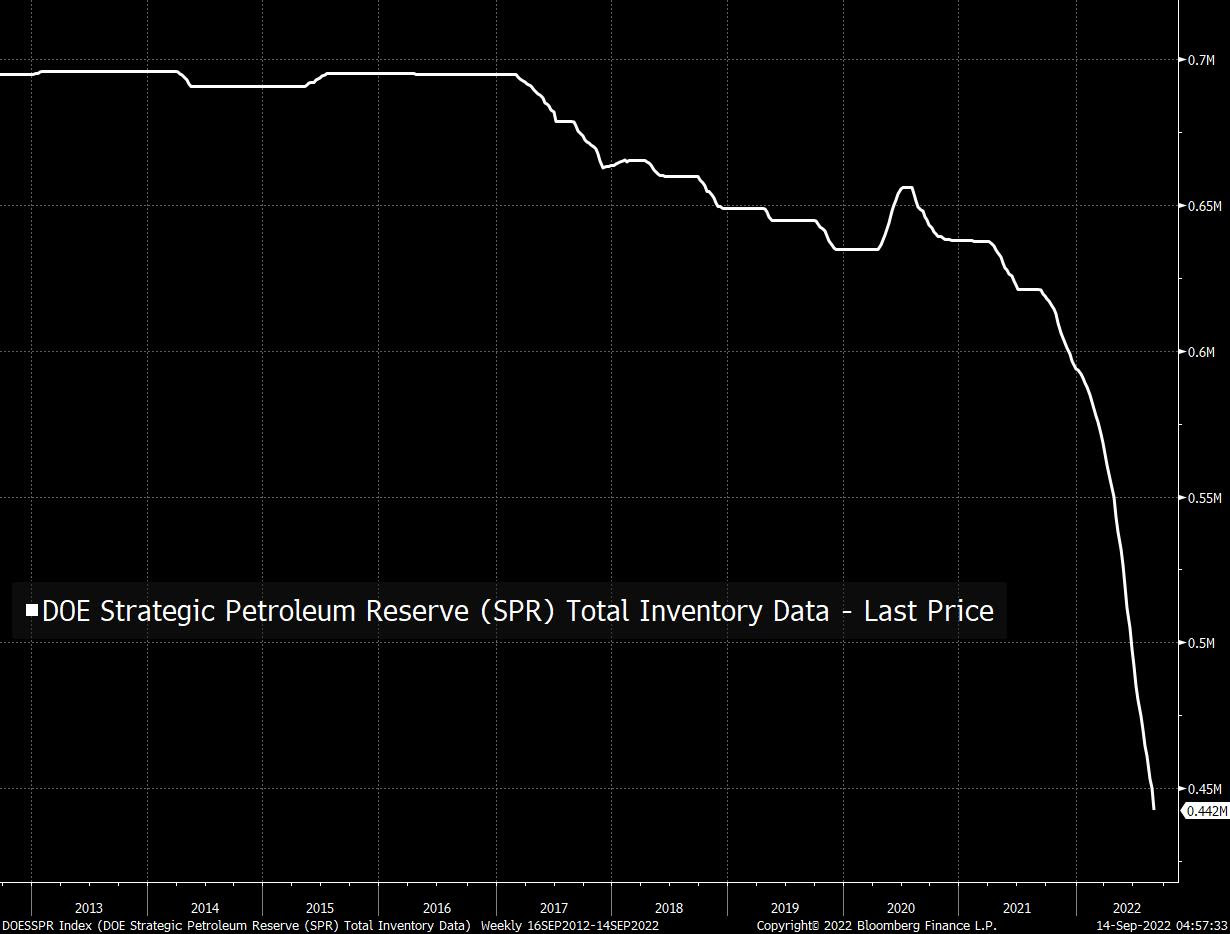

The Reserve-to-Consumption Ratio: Unlike the United States, which utilizes the SPR as a market stabilization tool, China views its reserves as a survival mechanism for state continuity. Current estimates suggest China holds between 80 and 90 days of net imports. However, this figure is deceptive. It includes both government-managed sites and commercial storage. In a true blockade or high-intensity conflict involving Iran, the state would likely seize commercial stocks, yet the logistical friction of moving that oil from coastal storage to inland industrial hubs creates an immediate "internal supply lag."

The Iranian Discount Dependency: China is the primary beneficiary of Iranian "S-grade" or "light" crude, often rebranded through Malaysian or Emirati intermediaries to bypass sanctions. This trade is not just about volume; it is about margin. Private Chinese refineries (Teapots) have optimized their complex distillation units specifically for these discounted grades. If an Iran war halts these flows, these refineries cannot simply "hot-swap" to Saudi Extra Light or West Texas Intermediate without significant hits to their refining margins and potential equipment recalibration.

The Strait of Hormuz Chokepoint Risk: Roughly 15% to 20% of China's total crude imports pass through the Strait. While China has invested heavily in the Gwadar port (CPEC) and pipelines through Myanmar and Russia, these land-based routes lack the throughput capacity to replace VLCC (Very Large Crude Carrier) maritime volume.

Quantifying the Stockpile Burn Rate

To understand how long China can withstand a total Iranian supply disruption, we must apply a Stress-Tested Burn Rate formula. If we assume a total loss of Iranian barrels—approximately 1 to 1.5 million barrels per day (bpd)—the math shifts from "days of consumption" to "days of substitution."

- Total Import Requirement: ~11.5 million bpd.

- Iranian Component: ~10% to 13%.

- Inventory Drawdown Calculation: If China draws 1.5 million bpd from its SPR to cover the Iranian deficit, a 500-million-barrel reserve theoretically lasts 333 days.

This surface-level math fails to account for Secondary Contagion. A war in Iran rarely stays in Iran. If the conflict expands to involve Saudi or Emirati infrastructure, or if the Strait of Hormuz is mined, the deficit jumps from 1.5 million bpd to upwards of 5 or 6 million bpd. Under this "Contagion Scenario," China's 90-day reserve evaporates in less than 45 days as panic-buying and industrial hoarding accelerate the burn rate.

The Logistics of the Invisible Fleet

China's reliance on Iran is facilitated by a "dark fleet" of aging tankers. These vessels operate outside standard maritime insurance and Western oversight. In a high-intensity conflict, these tankers become high-risk targets.

The primary risk here is Insurance Decoupling. Even if China is willing to buy the oil and Iran is willing to sell it, the physical act of transport requires protection. China’s People’s Liberation Army Navy (PLAN) currently lacks the blue-water power projection to escort tankers through the Persian Gulf during an active war. This creates a "Security Gap" where the oil exists, the demand exists, but the bridge between them is structurally unsound.

The Refinement Bottleneck

Analysis of the SPR often ignores the chemical specificity of the stored oil. Crude oil is not a monolithic commodity. China’s reserves are a mix of heavy sour and light sweet crudes.

- Medium-Heavy Sour: Predominantly from the Middle East. High sulfur content requires sophisticated desulfurization units.

- Light Sweet: Often domestic or sourced from Russia/Africa.

If the Iranian conflict removes light crude from the market, Chinese refineries must process heavier, more "difficult" barrels. This increases the Energy Intensity of Refining, effectively reducing the net energy gain of every barrel processed. This is a hidden tax on the Chinese economy that standard GDP projections fail to capture.

The Displacement Effect and Global Re-Routing

When Iranian supply drops, China must compete on the open market for Atlantic Basin crude or increased Russian ESPO (Eastern Siberia-Pacific Ocean) flows. This triggers a Global Displacement Cycle.

- Price Arbitrage Destruction: China loses its $5 to $10 per barrel discount on Iranian oil, forcing it to spend more USD reserves.

- Russian Leverage Escalation: As China becomes more dependent on the Power of Siberia pipelines and Russian rail-borne crude, Moscow gains significant pricing power, potentially demanding payment in non-convertible currencies or strategic technology transfers.

- Freight Rate Spikes: The demand for non-Persian Gulf tankers skyrockets, increasing the landed cost of oil even if the barrel price remains stable.

Strategic Mitigations and Their Limitations

Beijing is not passive in this environment. They utilize three primary "Release Valves" to mitigate the impact of an Iranian war on their stockpile.

The Strategic Coal-to-Chemicals Pivot

China maintains the world's largest coal reserves. In a protracted oil crisis, the state can mandate a shift toward Coal-to-Liquids (CTL) technology. However, CTL is water-intensive and environmentally catastrophic. More importantly, it cannot be scaled fast enough to replace a 1.5 million bpd deficit in a quarterly timeframe. It is a multi-year mitigation, not a tactical fix.

Domestic Production Mandates

State-owned enterprises (CNPC, Sinopec, CNOOC) are under "Seven-Year Action Plans" to increase domestic output. Most of China’s easy oil is gone; what remains is in deepwater or complex shale formations (e.g., the Tarim Basin). These barrels have a high Marginal Cost of Production, often exceeding $60 to $70 per barrel. They act as a price floor rather than a competitive advantage.

Mandatory Demand Destruction

The most effective tool in the CCP’s arsenal is the ability to enforce immediate demand destruction. Through the "dual control" system of energy consumption, the government can simply cut power to non-essential industries or restrict private vehicle usage. This preserves the SPR for military and critical infrastructure but at the cost of massive industrial contraction.

The Logical Conclusion of the Conflict Calculus

The assumption that China is "ready" for an Iranian war because of its massive stockpile is a fundamental misunderstanding of energy logistics. The stockpile is a buffer, not a solution. The real-world constraint is the Maximum Sustainable Drawdown Rate. You cannot empty a 500-million-barrel reserve overnight; the physical infrastructure of pumps and pipelines has a hard ceiling.

If the conflict in Iran persists beyond a 90-day window, China faces a binary choice: either enter the conflict to secure maritime lanes (an overextension of current PLAN capabilities) or accept a managed economic recession to preserve the remaining 20% of the SPR for national defense.

The Strategic Play

For institutional investors and energy strategists, the indicator to watch is not the SPR volume, but the Refinery Run Rates in Shandong. When these independent refineries begin to de-stock or lower their utilization rates, it signals that the "Invisible Fleet" is failing and the Iranian discount is no longer outweighing the risk premium.

Strategically, the move is to hedge against the West-to-East Freight Spread. As China is forced to look toward the Atlantic and West Africa to replace Iranian barrels, the cost of shipping will decouple from the price of oil. Positioning in specialized tanker equities and LNG infrastructure—which serves as the primary substitute for industrial heating during oil shocks—is the only logical defense against a prolonged Iranian supply disruption.